1.1. From Debt Crisis to Asset Revaluation: The Next Financial Regime

This isn’t about collapse. It’s about how the system persists when debts can’t be repaid.

Welcome everyone to what is a new format here on my channel for presenting this information. I wanted to try something different because I’m aware that I can sometimes use too much jargon. My goal is to make this content as accessible as possible, even for those with no background in finance.

This presentation is the first of a three-part series. ch part will be split into two sections, with the second section appearing on my website. Together, these presentations represent six to seven months of deep research into the tokenization and unified ledger model and what it means for the economic future, looking 10–20 years ahead.

I believe this presentation may be the most important finance video you could watch this year. It aims to provide clarity on what is likely taking place in the financial system. I refer to this process as “The Great Revaluation.”

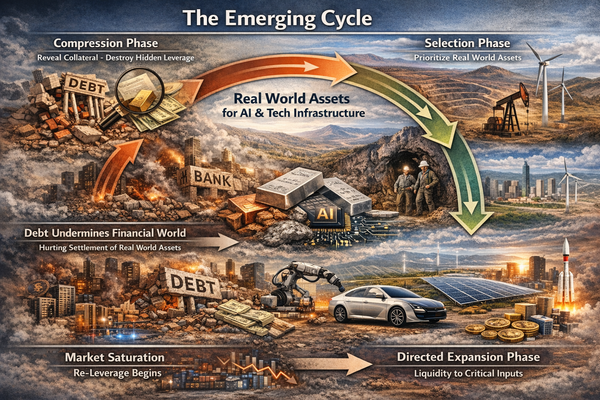

The presentation is structured around five main phases. The authorities do have a solution on the table, but it is a patch aimed at keeping debt serviceable while upgrading the asset side of the balance sheet. For example, the US Treasury Secretary has already indicated intentions to monetize the US balance sheet.

I am not presenting sensationalism. I do not believe we will see collapse, hyperinflation, a gold standard, or crypto evangelism. This is fundamentally a settlement and collateral story:

- Settlement means completing a trade—pay cash, receive goods, transaction is final.

The settlement problems reflects one of too many claim on too few assets.

- Collateral is the deposit or asset pledged to obtain lending.

And available collateral quality has deteriorated.

Historically, gold was the settlement device and collateral under the gold standard. Under Bretton Woods, the US dollar became the settlement standard, backed by central bank reserves and government bonds. Later, housing and securitized assets became part of the collateral system.

The new era is moving toward atomic settlement, where money and assets transfer simultaneously. Ownership moves instantly, reducing reliance on institutions and increasing trust in the assets themselves, recorded on blockchain.

The core question is: what backs the promises we’re asked to trust, and what happens when that backing weakens? Debt influences taxes, employment, personal freedom, and the assets you are allowed to own or pledge. Historic examples include the 1933 executive order on gold and increasing regulation on private property.

2. Why Debt Reduction Does Not Work

Debt reduction is ineffective in the current context. Consider debt-to-GDP ratios from 1900 to 2015—they are on an unsustainable trajectory. Gross government debt divided by nominal GDP shows debt growing faster than the economy can absorb.

- Unfunded liabilities such as healthcare and pensions will expand debt further.

- Inflation helps inflate nominal GDP, reducing the real value of debt.

- Boosting productivity could help, but today there is minimal real productivity growth, particularly in Europe.

- Globalized wage suppression and automation replace labor rather than expand it, limiting growth potential.

The core issue is that there are more enforceable promises than credible settlement assets. Extreme debt is fundamentally a settlement problem.

- Growth helps service debt; assets help extinguish debt.

- When debt grows faster than your collateral base, repayment becomes impossible.

- A trusted settlement instrument is essential to ensure asset value can clear debt.

Currently, the system survives by postponing settlements, rolling debt forward. High debt requires continual asset value increases; otherwise, the foundations of a debt-based economy erode.

3. The Collateral & Settlement Problem

Excessive debt means survival depends on liquidity (ability to generate cash inflows). Debt saturation is evident across Western nations with high public and private debt. Debts are rolled over, creating a growing refinancing risk.

Liquidity depends on credible, pledgeable collateral:

- Lenders will only lend if they receive reliable collateral.

- Collateral is required for short-term lending, bank credit, or central bank operations.

The problem today:

- Existing collateral is exhausted.

- New forms must be monetized.

- Promises exceed real assets; collateral exists but is harder to use.

- Settlement is too slow for today’s leverage; assets must be converted into cash before they are needed.

Example: US 10-year yields (1980–present) show falling yields due to sovereign debt buying. Quantitative tightening by central banks is slowly redistributing debt ownership, causing yields to rise, reflecting collateral deterioration.

The result: a collateral constraint, overissued sovereign bonds, highly leveraged housing, deteriorating credit quality, and difficulty accessing liquidity.

4. Historical Proof

A historical precedent is England, 1689. The government had debts it could not repay, and borrowing against future taxation was insufficient.

- Bank of England established in 1694, creating a permanent national debt backed by taxation.

- Land was used as collateral, revaluing its status and enabling borrowing.

- This released money into the economy without repaying debt, expanding liquidity through collateral revaluation.

Land prices rose from the 1680s into the post-Napoleonic era, increasing from 5–10% of GDP to 200% of GDP. Landowners were cash-poor but asset-rich, and revaluing land unlocked trapped liquidity.

A circular flow emerged:

- Land used as collateral for loans.

- Banks lent against land.

- Landowners transacted with merchants.

- The state taxed resulting economic activity.

The outcome: a liquidity boost without debt reduction, preserving leverage while financializing asset values.

5. Monetize the Assets

The solution today is to monetize the asset side of the balance sheet:

- Debts are growing faster than usable assets.

- Assets are opaque, slow to sell, and carry risk.

Tokenization addresses these issues:

- Converts hard-to-use assets into liquid, pledgeable forms.

- Enables real-time valuation and 24/7 collateral availability.

- Fractional ownership allows broader participation (e.g., partial house ownership).

- Atomic settlement enables instant ownership transfer.

Tokenization increases asset liquidity and accessibility, applying a liquidity premium, which can drive asset value appreciation. The process:

- Balance sheet repair without debt reduction.

- Existing assets are repriced to support debt, preserving leverage.

- Tokenized assets can be pledged as collateral, increasing system liquidity.

Economic consequences:

- Increased monetized economic activity.

- Faster transaction settlement and higher money velocity.

- More financial services opportunities, particularly for large intermediaries.

- Limited productivity growth, but nominal GDP expansion via asset liquidity.

The Great Revaluation: selective tokenization and collateralization of real-world assets to sustain heavily indebted economies. Asset value appreciation occurs via liquidity premiums, preserving system function without creating new wealth.

Glossary - The Great Revaluation

The Great Revaluation

A process where existing assets are re-priced higher to keep a heavily indebted financial system functioning. It does not create new wealth; it revalues what already exists, so debts can continue to be serviced.

Settlement

The moment a transaction is completed: money is paid, the asset is delivered, and the deal is final.

Settlement Problem

When there are more financial promises than real assets available to complete them. The system survives by delaying or rolling debts instead of settling them.

Collateral

An asset pledged to secure a loan.

If the borrower fails, the lender takes the collateral.

Collateral Quality

How reliable an asset is as security for lending.

Good collateral is liquid, stable, and widely accepted.

Liquidity

The ability to raise cash quickly without major loss.

An economy can have valuable assets but still suffer liquidity shortages.

Debt Saturation

When debt grows so large that new borrowing no longer produces real economic growth, and mainly serves to refinance old debt.

Refinancing

Replacing old debt with new debt when it matures.

Modern financial systems depend on constant refinancing to survive.

Atomic Settlement

A transaction where payment and ownership transfer happen at the same time, removing delays and counterparty risk.

Tokenization

Turning real-world assets (property, metals, infrastructure) into digital tokens that are easier to trade, pledge, or use as collateral.

Unified Ledger

A shared digital record where assets, ownership, and transactions are recorded in one system, often using blockchain technology.

Fractional Ownership

Dividing an asset into smaller pieces, allowing partial ownership and making illiquid assets usable as collateral.

Monetization of Assets

Using existing assets to generate liquidity without selling them, often by pledging or tokenizing them.

Liquidity Premium

An increase in an asset’s value because it is easier to trade or pledge, not because it produces more goods or services.

Balance Sheet Repair

Stabilizing the financial system by upgrading assets, not by reducing debt.

Leverage

Using borrowed money to increase exposure to assets.

Leverage amplifies gains — and systemic risk.

Nominal GDP

Economic output measured in current prices.

It can rise through inflation or asset repricing without real productivity growth.

Financialization

The shift toward treating assets primarily as financial instruments rather than productive or usable resources.

Trusted Settlement Asset

An asset widely accepted to finalize debts. Historically gold, then government bonds and currencies — today increasingly strained.